|

LISTEN TO AUDIO VERSION:

|

Balancing act between regulatory necessity and economic efficiency

Since January 2018, the mandatory minimum liquidity coverage ratio has been set to 100%. Stockpiling high-quality liquid assets, however, has immediate economic consequences: the lower return on these assets is an additional burden on the already limited earning power of financial institutions in the persistently low interest rate phase. The balancing act is to keep the LCR slightly above the minimum ratio and to maintain this at all times. Audits also show the understandable expectation of the supervisory authority whereby a higher LCR volatility also results in a higher internal LCR limit.

An efficient LCR management therefore requires an LCR which is as stable as possible and has a high LCR forecast quality. Assessing the LCR volatility must also take into account intra-month effects which, in our experience, and especially in many smaller institutions, is only carried out to a very limited extent. The natural volatility of the LCR depends on the institution’s specific business model as well as the product structure and design. In practice, however, we often observe that some institutions, especially smaller ones, have only implemented basic LCR forecasting or none at all. But even larger institutions experience considerable problems in achieving a sufficient forecast quality. Forecasting the LCR with artificial intelligence (AI) enables a significant improvement in LCR forecast quality and consequently LCR management.

Significant positive effect on profit when using AI for LCR forecasting

Using AI for LCR forecasting offers three major benefits:

- Economic benefit

The primary economic benefit results from the fact that more accurate LCR forecasting allows the selection of a lower internal target LCR while ensuring compliance with the minimum liquidity coverage ratio. Reducing the portfolio of LCR-eligible assets enables higher-return investments and the early initiation of management measures. A longer planning horizon expands the universe of possible management tools and generates cost advantages for the selection and implementation of measures. - SREP assessment and regulatory requirements

According to MaRisk[2]and ILAAP[3], institutions are obliged to both identify liquidity squeezes at an early stage and forecast their development. Using AI increases the accuracy of LCR forecasts, which in turn allows institutions to adjust the LCR according to their internal LCR limit, thus reducing LCR volatility. Both aspects therefore have a positive effect on the normative perspective of ILAAP within the SREP[4].

- AI experience as a competitive advantage in digital transformation

The use of artificial intelligence is an essential part of the banking sector’s digital transformation process. Among other regulators Germany´s supervisory authority BaFin[5] has also come to the same conclusion, as it increasingly deals with the topic itself and has signaled a clear interest and openness with regard to the most diverse areas of application. It is therefore important that banks keep abreast of developments and address the issue of artificial intelligence. They can, however, only succeed with the help of concrete use cases. Early adoption of AI is therefore likely to constitute an important competitive advantage.

In order to illustrate the economic benefits, the earnings potential was approximated with a simplified calculation example in Figure 1.

Figure 1: Economic benefit—earnings potential of a model bank

Figure 1: Economic benefit—earnings potential of a model bankIn the initial situation, the institution does not apply LCR forecasting, has an own investment portfolio of EUR 1.6 billion, liquid assets of EUR 1.5 billion, an internal LCR limit of 140% and a current LCR of 150%. In this situation, the total return, i.e. the combined return from the own investment portfolio and deductible central bank reserves, amounts to EUR 11 million. The institution then follows an experience-based approach (method 1). Based on historical data, they determine a forecast error of 15% in the experience-based estimate of net cash outflows. In order to ensure that the bank will meet the internal LCR limit, even in the event of an expected net outflow of 115% of the current net outflow, they must hold an additional EUR 110 million in liquid assets. This reduces the total return to only EUR 8 million.

By using AI-based LCR forecasting, the institution is able to reduce the forecast error to 2%. Consequently, they only have to anticipate an expected net outflow of EUR 1,02 billion and therefore hold fewer liquid assets (method 2). The release of liquid assets results in a 17% higher total return. Since the uncertainty of forecasts has been reduced, the institution can now reasonably justify a reduction of the internal LCR limit from 140% to 120% (method 3). This leads to a lower demand for highly liquid assets and thus to a reallocation towards higher-yielding, non-LCR-eligible assets, which in turn generates a higher return.

LCR buffer optimisation (method 4) using AI offers further optimisation potential. This allows banks to optimise the buffer structure (level 1, level 2A, level 2B) and select assets per LCR level. In the calculation example we assume the average portfolio return to conservatively increase by a half percentage point, resulting in an increase in total return to EUR 22 million.

Notwithstanding the highly simplified example, the optimisation and earnings potentials are evident. Various projects have demonstrated the successful use of AI to optimise forecasts (e.g. to model prepayments). Thus, LCR forecasting represents an ideal application area for AI. In addition to the pure forecast based on ordinary business activity, the ideal target solution for LCR forecasting should also include the possibility of simulating LCR management measures as well as transactions with a significant impact on the LCR.

Process model as a critical success factor for AI applications

While the simplest forms of AI are designed to derive parameters from data and a given model (e.g. regression model), the more complex models of machine learning and deep learning do not specify any rules, but only provide data from which the AI derives the model itself. As shown in Figure 2, the term “artificial intelligence” includes all forms of machine learning that attempt to emulate human thought patterns. Machine learning and deep learning can be regarded as AI subcategories.

Figure 2: Classification of AI

Figure 2: Classification of AIA further classification of AI methods results from the nature of the “learning problem”. While the goal of supervised learning methods is to generate a predefined output (e.g. value, category, etc.) from a given input according to certain specifications, the focus of unsupervised learning methods is on understanding data. Clustering, for example, does not involve the prior definition of groups (see examples in Figure 3).

Figure 3: Further classification of ML methods

Figure 3: Further classification of ML methodsThe zeb process model[6]has already proved its worth in developing AI applications, and it quickly reveals positive results. A narrow functional scope of the use case has proved to be essential to success. Subsequently, the model develops hypotheses on the influence of different variables on the LCR’s future development. With regard to the structural framework, we must also examine the extent to which required data is available in a suitable data structure and legally usable. On the basis of the selected data, the appropriate methods are narrowed down, and their concrete results are then compared in a beauty contest. The valuation reference for the forecast quality either uses historical data or the results of an existing approach. In addition to the forecast quality, criteria such as traceability, model usability, and implementation effort must be considered.

Bank-specific evaluation of the LCR forecasting approach necessary

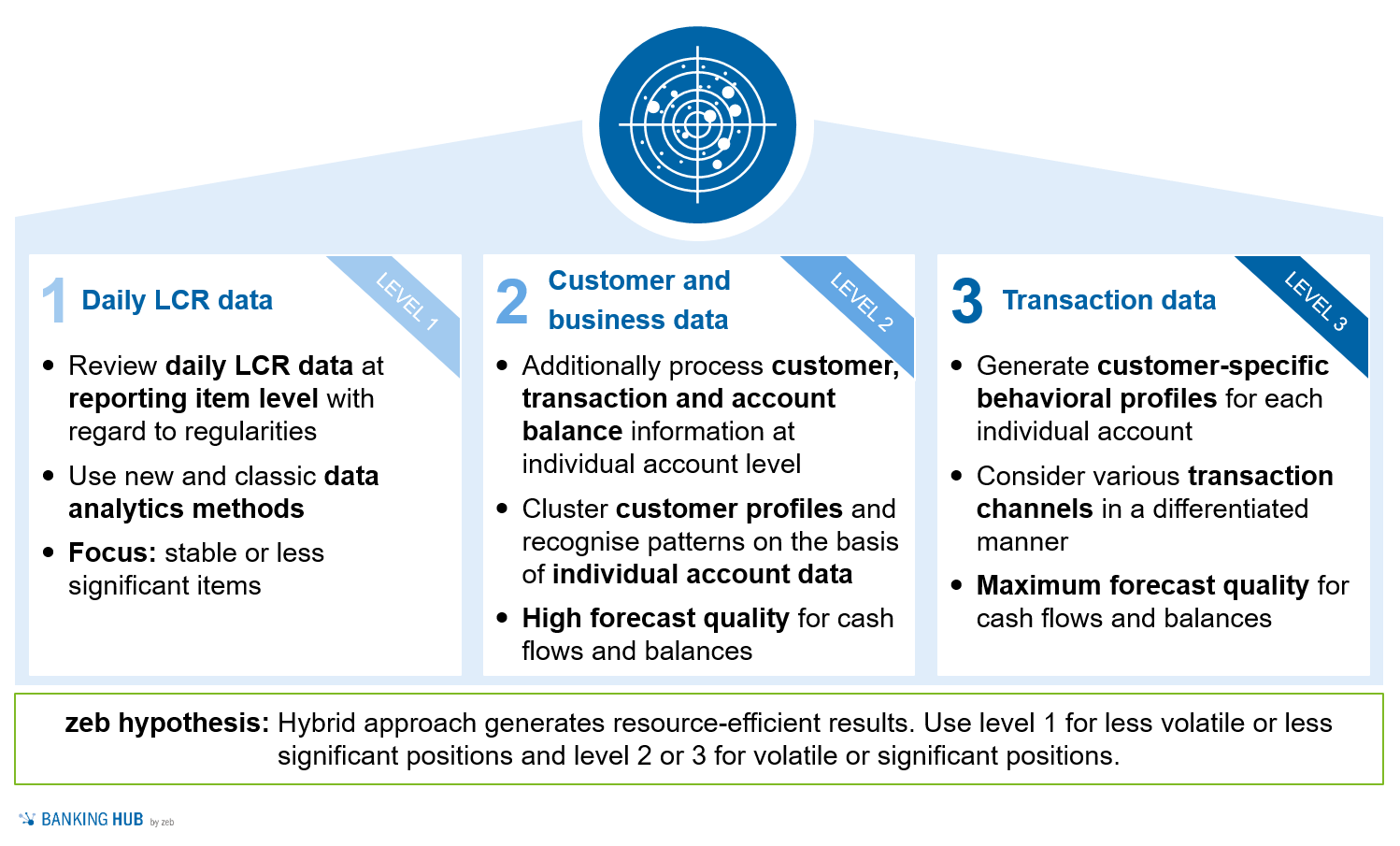

Figure 4: LCR forecasting levels

Figure 4: LCR forecasting levelsTaking into account bank-specific requirements, the nature and complexity of the business model and the available resources, different levels of LCR forecasting with AI are conceivable. These levels differ in terms of data granularity and the modeling approach used. Figure 4 gives an overview of the different levels of LCR forecasting, whereby the next level always includes the analysis of data from previous level(s).

Level 1: daily LCR data

As a rule, institutions can already generate a basic LCR forecast on the basis of regulatory reporting templates. This requires daily values of the reporting positions from the reporting templates C 72.00 to C 76.00 for an extended time period, e.g. three years. The forecast quality can be improved by adding data from single transactions to the data basis, if available.

An analysis of the time series of individual reporting positions can, for example, identify cyclical patterns. Seasonal fluctuations are caused by regularities, such as increasing consumption during the Christmas season. Further patterns result, for example, from monthly rhythms for credited salaries or debited rent payments.

In addition to classic methods, such as linear regressions, modern data analytics methods are also available to identify the regularities. Compared to conventional methods, modern methods are better able to detect seasonal effects in particular. However, the forecast quality of a model depends highly on the input data. Since this is only available in highly aggregated form in level 1, the advantage compared to classic methods is often limited.

Level 2: enhancement with customer, account and market data

To improve the LCR forecast quality, the level 2 analysis is supplemented with customer data (age, income, credit scores, etc.), account data (balances, limits, etc.) and market data (interest rates, GDP, etc.).

Customer and account information makes it possible to derive customer profiles based on behavioural attributes and to group customers into homogeneous clusters. Learning the usual cash flow profiles of these clusters can significantly increase the forecast accuracy. Furthermore, it is also possible to anticipate migrations between SME retail and SME wholesale customer categories. In addition to internal bank data, the analysis can also include external market data. For example, the interest rate level, yield curves or even GDP are relevant influencing factors and enable a further improvement of the LCR forecast quality.

Level 3: enhancement with transaction data

The level 3 analysis also considers transaction data. Information, for example on the transaction channel (credit card, debit card, direct debit, etc.), the payment category (wages/salary, mortgage, consumer spending, etc.) or customer contact information, such as a credit offer, may be of interest. Machine learning can be used to categorise the transaction data (e.g. payment patterns), enabling the identification and anticipation of changes in customer behaviour. In contrast to level 2, the model is trained at individual customer level. This allows the user to forecast balances and cash flows for each individual account and to achieve maximum forecast quality.

Level 3 does not per se represent the optimal target image for LCR forecasting. Instead, zeb recommends a hybrid approach that balances the advantages and disadvantages of the various levels in an optimal and resource-efficient manner. To a large extent, institution-specific features together with the volatility and significance of the individual LCR positions determine the selection of the granularity level.

LCR management with AI-based LCR forecasting provides cost and competitive advantages

AI-based LCR forecasting enables banks to realise substantial earnings potential and significantly improve risk management. Automated LCR forecasting also relieves the burden on risk management resources and is highly flexible. In addition to integrating historical data, LCR forecasting can also be supplemented with scenario data to simulate previously unobserved developments (planning assumptions, black swan events, etc.). Such AI use cases are an essential part of the digital transformation and an important basis for the banks’ future competitiveness.

One response to “LCR forecasting with AI”

Tony Devine

A really informative article and so well described and written, some really serious considerations within, supported by expert and professional analysis.