|

Getting your Trinity Audio player ready...

|

|

LISTEN TO AUDIO VERSION:

|

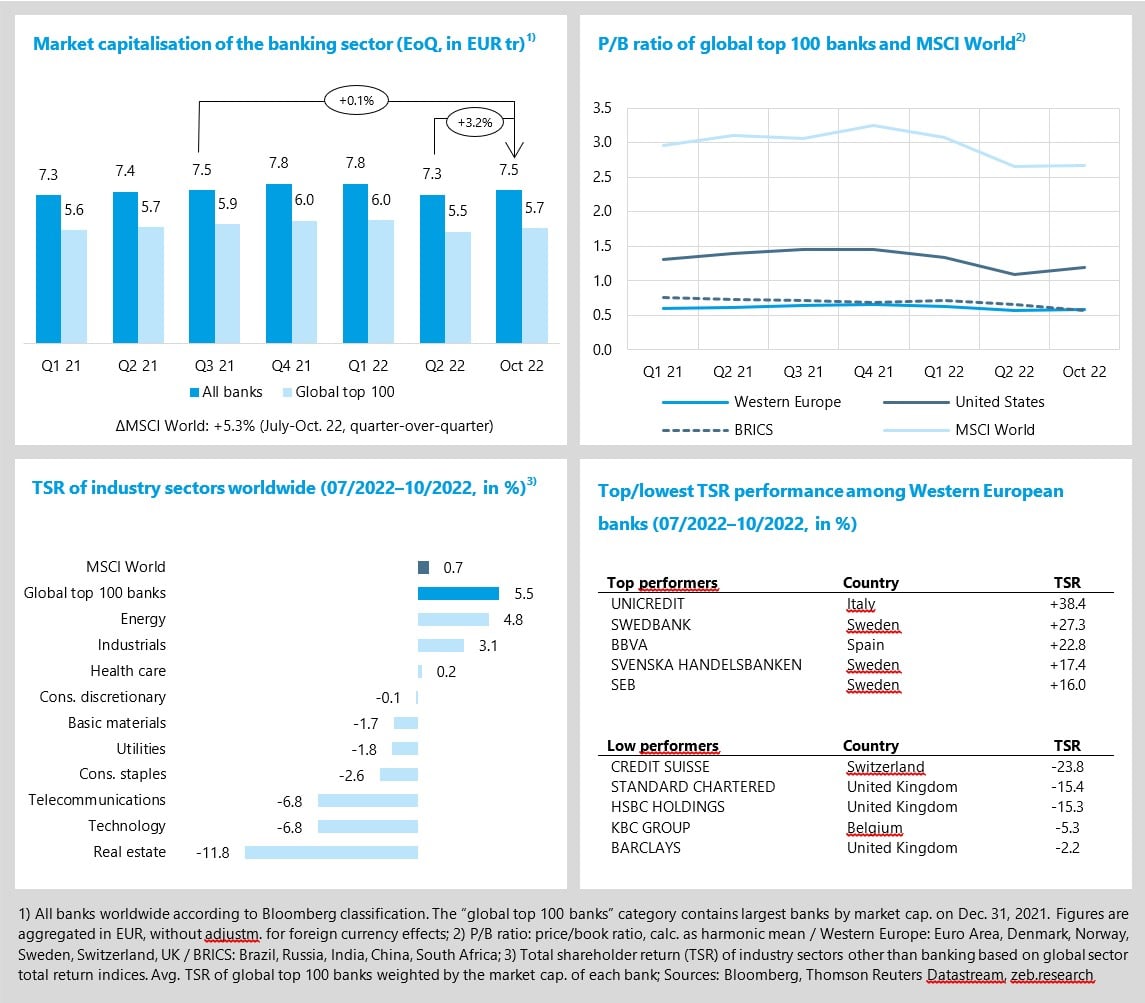

Bank stocks beat all other sectors in Q3 2022

+5.5% QoQ TSR performance of global top 100 banks

- After significant corrections in Q2, TSR of the MSCI World stagnated at +0.7% in Q3 2022 – real estate and technology were the lowest performing sectors.

- Global top 100 banks outperformed the market and all other sectors – driven by U.S. (TSR +11.9% QoQ) and Western European banks (TSR +4.3% QoQ).

After significant corrections on global capital markets in the second quarter of 2022, markets stagnated in the third quarter (MSCI World TSR +0.7% July-Oct. 22, market capitalisation +5.3%). Global top 100 banks outperformed the market and all other sectors in terms of TSR performance (+5.5% July-Oct.) – further interest rate increases contain more advantages than disadvantages for banks, most Q3 results were better than anticipated by analysts, and high levels of state support keep provisioning levels low – for now.

- TSRs of S. banks were hit particularly hard in the first half of 2022 with -23.9% – their recovery from July to October 2022, however, was the strongest across regions (+11.9%, Western Europe: +4.3%, BRICS: -3.8%). P/B ratios of Western European banks stabilised at 0.58x (+0.01x), while those of U.S. banks partially recovered by +0.11x to 1.20x – still significantly lower than a year ago (Q3 2021: 1.45x). BRICS banks: 0.58x (-0.08x).

- Among the top performers in terms of TSR, the Energy sector with +4.8% QoQ is once again performing very well. Looking at capital market performance YTD, the Energy sector is the only one with positive total shareholder return (TSR of +22.0% YTD) – all other sectors show negative TSRs that are often in the double digits.

- Looking at individual European banks, Credit Suisse is under pressure after public scandals (settlement for tax fraud and money laundering in France), losses due to the collapse of Archegos and Greensill as well as a Q3 22 loss attributable to shareholders of CHF 4.0 bn. UniCredit is topping the list of Western European top performers with a TSR of +38.4% QoQ – the bank significantly outperformed analyst expectations in Q3 22 (best quarter in a century) by profiting from higher interest rates and unexpectedly low credit losses.

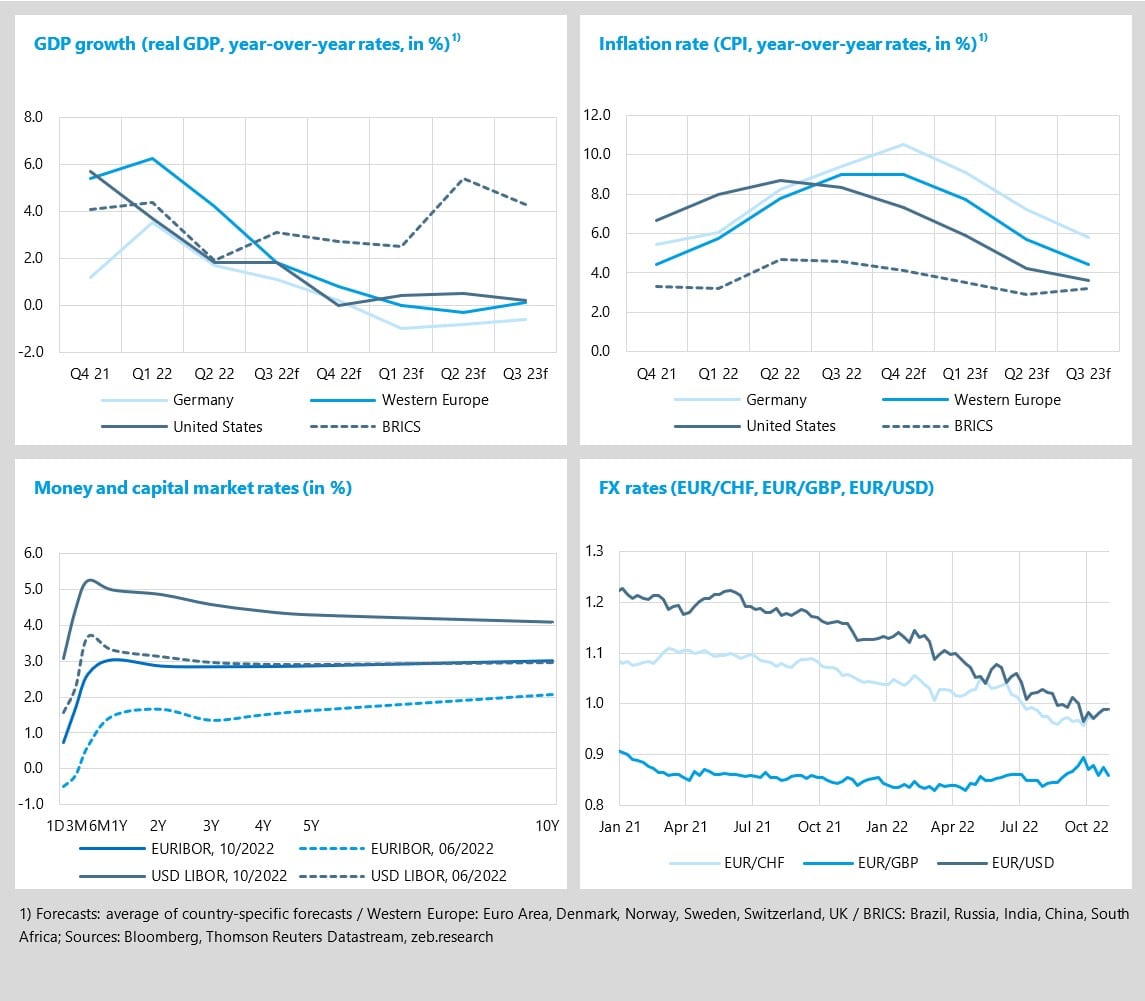

Recession is looming and central banks continue to fight inflation

-1.0% YoY expected real GDP growth in Q1 2023 in Germany

- The global economic environment further deteriorated in Q3 2022 and a recession in Western Europe and the U.S. in 2023 is highly likely.

- Record-high inflation rates continue to drive medium- to long-term interest rates upward and force central banks to keep raising their rates.

Economic growth is dampening significantly across the globe and a recession, at least in Western Europe and the U.S., is unlikely to be avoided. Inflation rates remained extremely high in Q3 22 YoY (U.S: 8.3%; Western Europe: 9.0%; Germany: 9.4%), except for the BRICS region (4.6%), forcing central banks to continue their decisive fight against inflation by further raising interest rates. The more decisive actions of the U.S. Fed compared to the ECB, coupled with a harsher impact of the Russia-Ukraine war on Euro area economies, caused a further deterioration of the EUR/USD FX rate. To a certain degree, U.S. Fed’s task to bring down inflation is slightly easier than that of the ECB – U.S. inflation is mainly demand-driven, and core inflation levels are lower.

- For Germany, GDP growth rates are now expected to remain negative for the first three quarters of 2023. Western Europe is expected to see its low in Q2 23 (-0.3% YoY) and the U.S. in Q4 22 (0.0% YoY).

- Only in the U.S., inflation already seems to have hit its peak in Q2 22 with +8.7% YoY, as it dropped to +8.3% YoY in Q3 22 and is expected to further drop during 2023. For Germany, a peak in Q4 22 of +10.5% YoY is expected, and Western Europe is expected to plateau on its Q3 22 level of +9.0% YoY in Q4 22. The U.S. Fed as well as the ECB continue their relentless fight against inflation by continuously raising key interest rates (ECB by +75bp on October 27, 2022; U.S. Fed: +75bp on November 2, 2022). Markets expect further increases at upcoming central bank meetings – U.S. Fed: December 14, 2022 / ECB: December 15, 2022.

- The Euro remains under pressure as geopolitical uncertainties add a risk premium and ECB’s rate hikes are less decisive than the U.S. Fed’s. Throughout October 2022, EUR/USD remained below parity further fuelling inflation, as goods and commodities – such as oil – are often paid in USD and have therefore become significantly more expensive for European buyers.

Compared to a very strong second quarter 2021 that benefitted from positive catch-up effects after the COVID-19 crisis, profitability of U.S. and European banks is down YoY in Q2 2022 (ROE: -4.3%p and ‑1.2%p, respectively). The massive rise in interest rates led to higher net interest income figures at almost all institutions. However, this positive effect was more than fully offset by lower income in investment banking, an overall higher cost base, and higher credit risk provisions. Especially U.S. banks already started to prepare themselves for the impacts of a looming recession by increasing their loan loss provisions in Q2 2022 (+17bp QoQ, +44bp YoY) slightly dampening their profitability.

- Western European banks reduced their cost-income ratio by -4.1%p YoY to 61.0% (U.S. banks: +1.7%p, BRICS banks: +1.6%p). Revenues grew considerably by +13.6% YoY (U.S. banks: +13.6%, BRICS banks: +13.2%) beyond already higher, inflation-affected costs (+6.5% YoY, U.S. banks: +16.8%, BRICS banks: +19.5%).

- In Q2 2022, S. banks continued to increase their loan loss provisions considerably (+10 bp QoQ, +37 bp YoY) to prepare for potential losses due to the looming recession. Western European banks did not further increase their provisions (-1 bp QoQ, +9 bp YoY). As the worldwide economic outlook further deteriorates, additional increases in loan loss provisions in Q3 2022 can be expected.

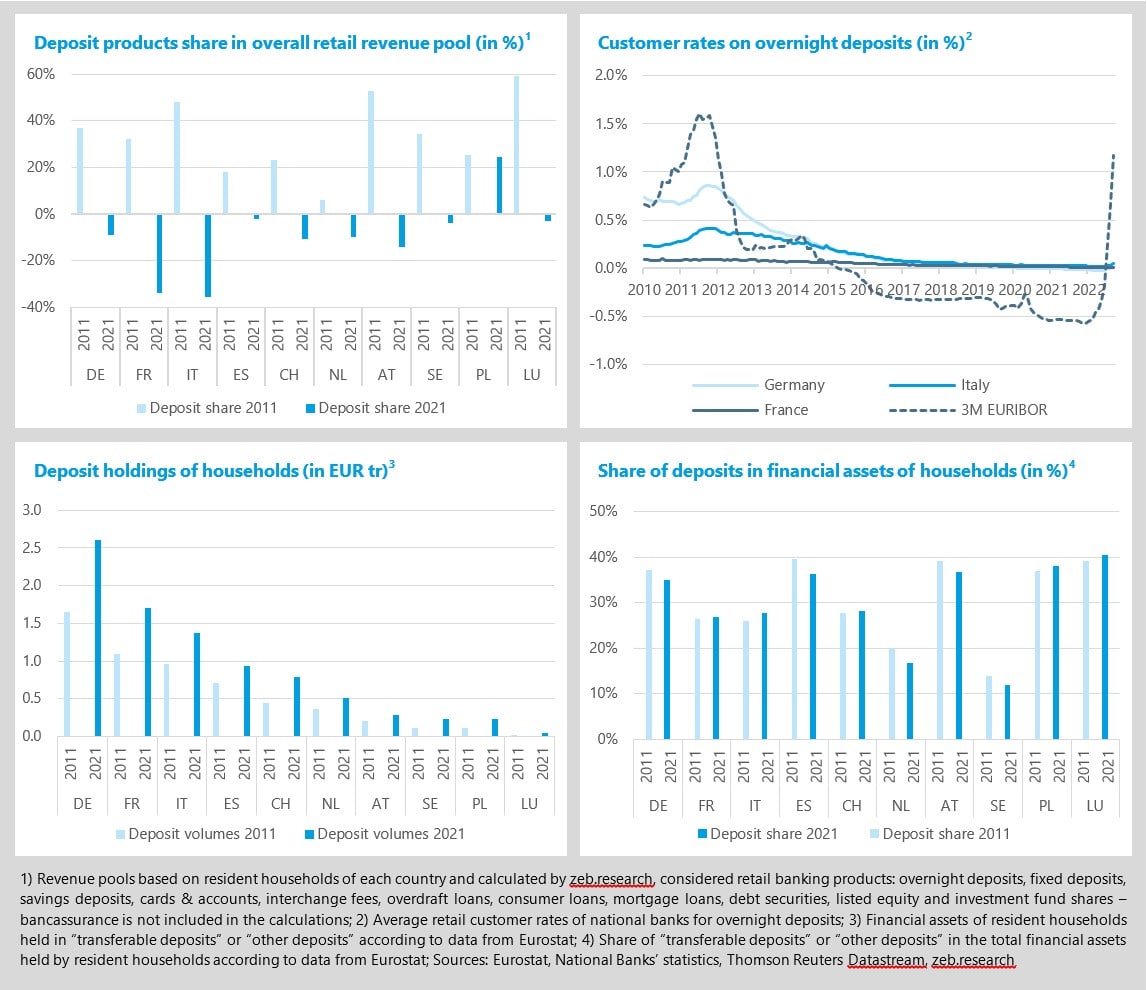

- Customer interest rates continue to follow the significantly heightened market yield curves and reached new highs across all products at the end of September 2022. Especially, mortgages are significantly more expensive than a year ago at 2.84% (+1.59%p YoY). Compared to credit products, banks are still relatively reluctant to pass on higher market rates to deposit holders (+0.41%p YoY to 0.56%). With positive yields, however, deposits once again become attractive to risk-adverse households and as cheap financing options for deposit-taking institutions – significantly more competition around deposits than during the zero-interest rate period can be expected. For more details see our special topic “rebirth of the deposit business”.

Special topic: rebirth of the deposit business

New and challenging environment

- With the end of the zero-interest rate regime, banks are now operating in a new and challenging environment – one of the positive effects from the banks’ perspective is the return of deposit products as a revitalised revenue stream.

- How did the deposit business fare in the past, how will it develop and what is the current playing field across Europe? Is a “battle for deposits” looming?

Soaring inflation ended the trend of falling interest rates and swiftly ended the zero-interest rate regime with an actual “Basel II interest rate shock”. As detailed in chapters one and two, banks are now operating in a new banking regime that is marked by significantly higher yields, growing recessionary trends, high uncertainty, volatile capital markets and geopolitical tensions.

For banks, this has a multitude of effects. Rising credit rates hamper the previously strong demand and an increase in credit risks is highly likely in the near to medium future. Inflation significantly pressures the cost base of banks. Volatility increases market price risks, and the 2022 downturn of equity and bond markets will cause higher securities write-offs – at least in 2022. Of course, there are also positive effects for banks operating in this new regime. If well steered, treasury might be able to generate sizeable profits again and most importantly, deposit products will become attractive refinancing and revenue generating products again. In this editions’ special topic, we put a spotlight on the rebirth of the European retail deposit business – how did it fare historically, how will it likely develop and what is the playing field in terms of market size, but also competition.

We analysed ten selected European retail markets[1] in detail by looking at the balance sheet of resident households, pairing it with price and margin computations to calculate retail revenue pools for these markets to answer the question “How much revenues can be generated with different retail banking products[2] in a given country and year?”. In 2011, before the zero-interest rate regime, deposits contributed approximately a third to the overall revenue pool across analysed countries – ranging from just 6% in the Netherlands to 59% in Luxembourg. Ten years later, however, contribution plummeted across markets to being a negative burden of approximately -13%, on average – except for Poland which only experienced a low, but not zero-interest rate environment. While overall revenue pools remained stable due to endless efforts to grow loan and fee-generating business activities, deposits turned from a highly profitable product to a cost factor in less than a century.

Now that interest rates are up again, banks can look forward to a trend reversal – at least to some degree. Assuming current implicit forward rates, the deposit business will become profitable again rather quickly and can be expected to contribute double digit shares to overall growing retail revenue pools across countries in the short to medium term. Just how profitable the deposit business is going to become again, depends on various factors. The pass-through rate of European banks, the (past) investment horizon of banks as well as the behaviour of customers will determine profitability.

Historically and on average, European banks have assumed an approximate 50% pass-through to their depositors – significant differences across markets can be seen, however, if one considers the different levels of overnight deposit customer rates observed in the period prior to the zero-interest rate regime. The slow and moderate incline in deposit rates that can currently be observed indicates a more cautious approach taken by European banks this time. Empirical evidence from Czechia also supports this notion: policy rates there were recently increased by 550 bp resulting only in a 20% pass-through.[3]

Another factor is the (past) investment horizon of banks. In some markets (e.g. Germany), a sizeable share of overnight deposit holdings by customers are traditionally used by most banks to invest in long-term products like interest rate swaps (up to 10 years) to generate secure, calculable and low-volatility returns with the portion of deposits that is likely to remain with the bank for long periods (“Bodensatztheorie” in German). In other markets (e.g. Poland), deposit investments as well as loan refinancing activities only consider horizons of a maximum of three months. Of course, banks following the latter approach can expect a more direct impact to their top-line results than banks with a longer investment horizon that put more emphasis on smoothing their returns.

Probably the biggest factor, however, will be the behaviour of customers, which itself is influenced by various determinants and structurally varies across markets. First, markets vary significantly in size. Not surprisingly, the largest economies of our sample, Germany and France, also represent the largest retail deposit markets in terms of volumes, with EUR 2.6 tr and EUR 1.7 tr, respectively in 2021. Households’ inclination towards putting their wealth into deposits is, of course, another factor influencing the overall deposit volumes across markets. Looking at the total financial assets held by households, only 28% are held in deposits by Swiss households, 17% in the Netherlands and only 12% in Sweden. In Luxembourg (40%), Poland (38%), Austria (37%), Spain (36%) and Germany (35%) deposits play a far more significant role in terms of their share in the national financial assets of households. Second, it remains to be seen how the capacity of households to accumulate savings amid soaring inflation rates will develop in the quarters to come. And where will the households put their remaining savings – into deposit, investment or insurance products? Third, one must keep in mind that the deposit market has changed significantly when it comes to its size, but also its competitive landscape.

Before the zero-interest rate regime, there were mainly traditional banks competing in often national markets. Since then, the number of market players has increased and the players themselves have become much more diverse. Today rather small providers of specialized financing, neo and online banks have taken the lead in offering interest rates on deposits (e.g. ING, German DKB, C24 or Klarna). On top of that, the battle for market shares is now being fought throughout Europe (or even globally). Platforms like Weltsparen allow customers to conveniently put their deposits with banks from virtually any country in Europe – making it easier to find the best offer.

Overall, the deposit business is experiencing a renaissance with the private customer business segment profiting the most. The sudden increase in profitability, however, is also likely to increase competitive intensity in the business – both from established and new market players. A “battle for deposits” is looming with potential cash outflows threatening the earnings turnaround. European banks will have to find the right balance between offering attractive returns to their customers while keeping their margins as high as possible. A good pricing strategy, customer communication and a trained sales force will be of paramount importance.