|

Getting your Trinity Audio player ready...

|

In order to meet these and other regulatory requirements and to be able to derive political, societal and institutional impulses for a sustainable economy in the future, corresponding data must be collected and made usable for the entire lending process. This entails the development of data request concepts, suitable data management tools, and a significant expansion of ESG data storage.

The concrete implementation of the extensive requirements poses functional, processual and technical challenges for financial institutions. One of the main tasks will be to make corresponding adjustments to the lending process and to anchor them in the respective core banking systems. In the following sections, we are taking a closer look at the specific impact of ESG data requirements on operational lending:

- Which ESG-specific data is relevant and how can it be collected?

- What data pools can be identified along the lending process and how do they impact the individual organizational units?

- What technical and process-related adjustments need to be made in the operational lending business?

Setup of an ESG data repository

In order for institutions to assess the scope of requirements for their operational lending business, they need to know what data needs to be collected and how this can be accomplished. However, the type and level of detail of ESG data that institutions need to collect from their customers depends on a number of factors, such as the type of lending transaction or the size and specific ESG risks of the borrower. For example, much more detailed information needs to be collected for complex corporate exposures than for “simpler” retail loans.

In general, the data infrastructure should have as high a level of detail as possible so that specific information on individual borrowers, loans and collateral can be recorded and subsequently processed. The data must also reflect the fact that ESG factors are highly future-oriented. This is evident, for example, in the case of physical climate risks. Assessing those requires scenario data for the next few decades.

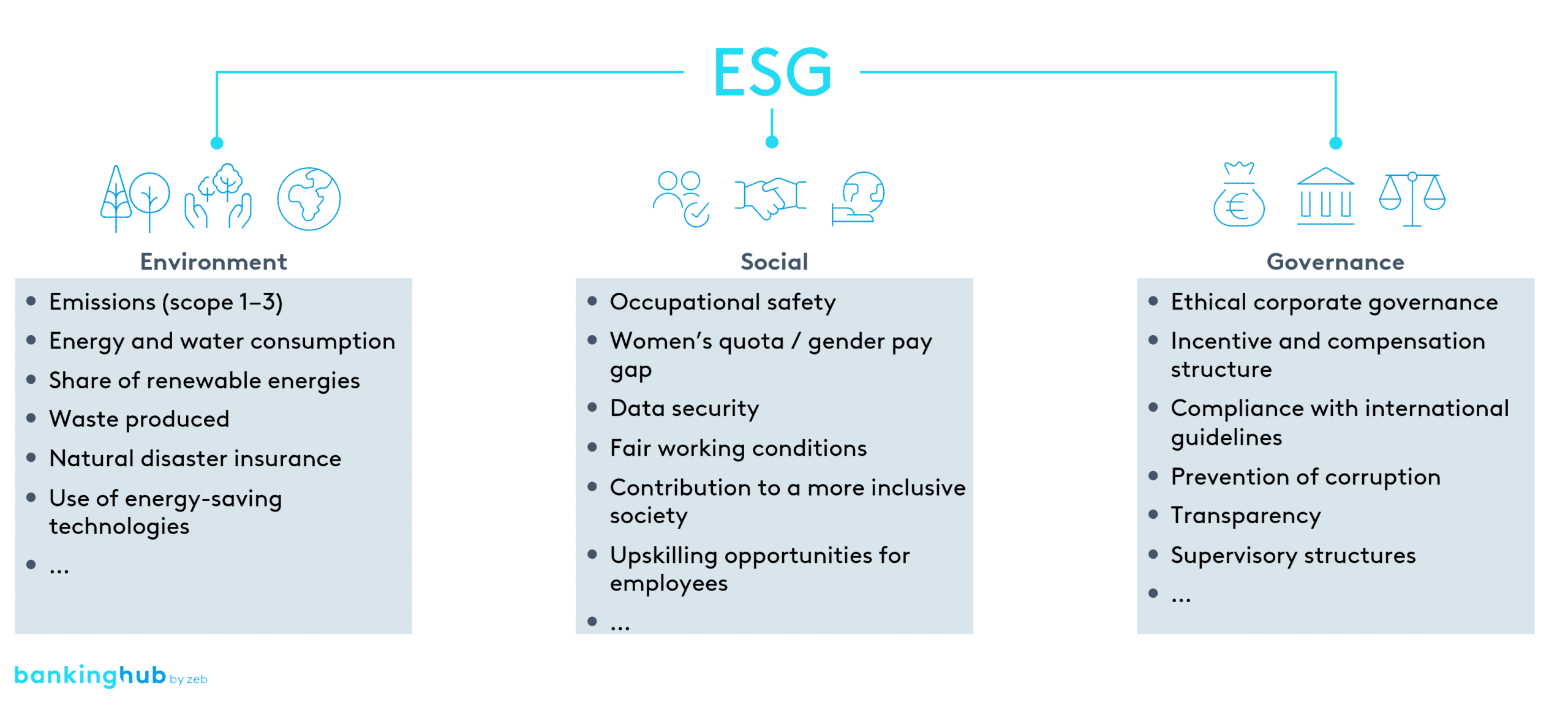

Current regulation focuses primarily on environmental and climate issues (The E part of ESG).[1] In this context, banks must collect information on a customer’s environmental footprint and what measures they take to minimize this impact. Figure 2 provides insight into some of the ESG data related to corporate customers.

In addition, further macroeconomic or scientific data such as climate scenarios and trajectories are required, particularly for risk management/controlling analyses, in order to generate effective steering impulses.

At least for large corporate customers, some data is already available publicly or through links to external databases/providers. In the case of medium-sized and smaller customers, however, institutions are faced with the task of collecting this information in the highest possible quality and yet efficiently through customer surveys or other instruments. Upcoming regulatory initiatives, in particular the CSRD[2], are expected to gradually improve the data situation (in terms of quantity and quality).

On the whole, institutions should embrace the opportunity of collecting customer-related ESG data and, especially at the outset, view it as a differentiating factor and a way to provide more targeted support to their customers.

ESG data pools along the lending process

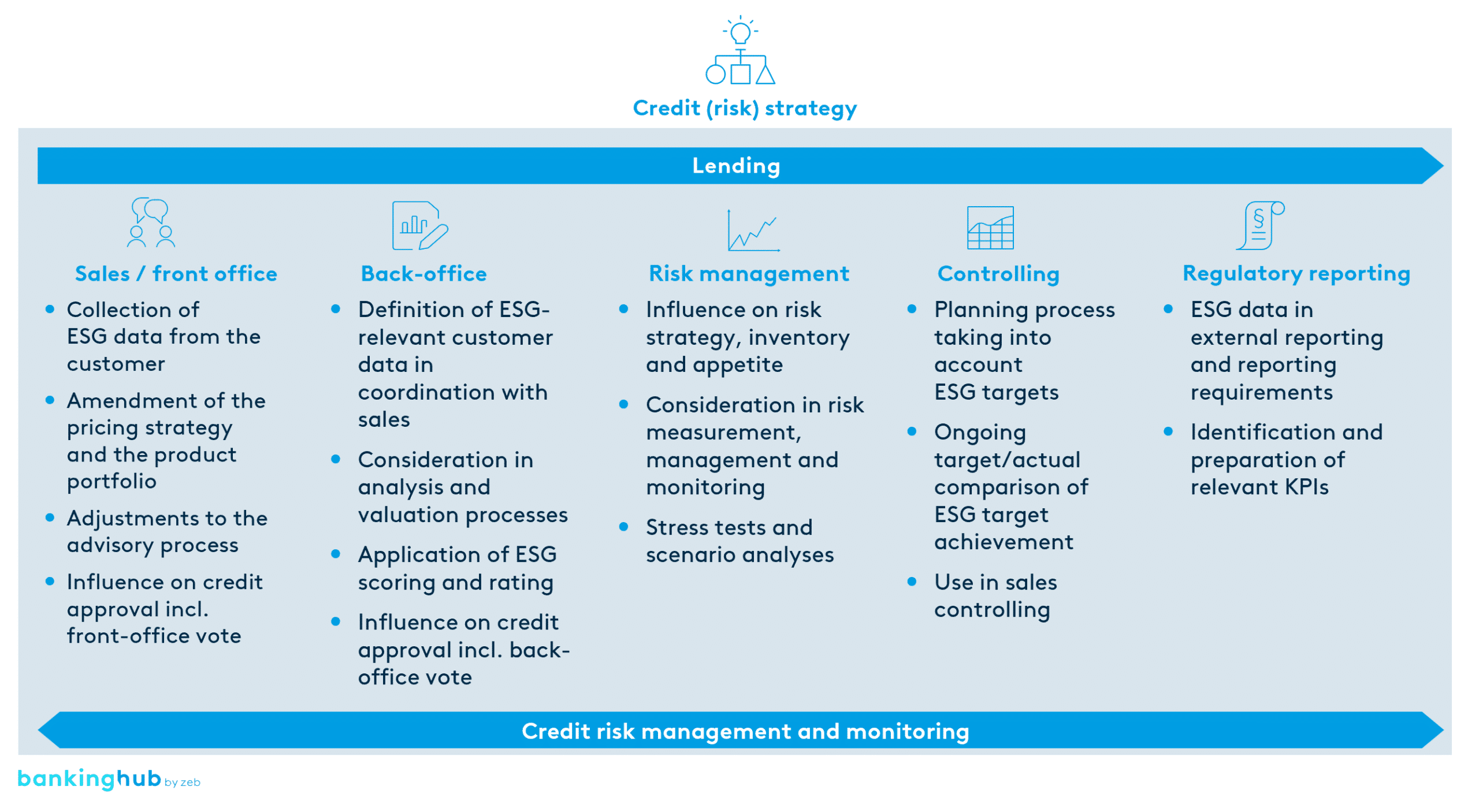

Various data pools are created in in line with regulatory requirements within the different organizational units of the operational lending business, which need to be populated with ESG-specific data.

Basically, ESG data must be anchored in the underlying credit (risk) strategy and integrated along the entire lending process. This ranges from the initial collection of data in the front office by sales staff, through analysis and approval processes in the back-office, to risk management. In addition, the data collected must be incorporated into controlling and processed for reporting purposes. In this context, it must be continuously taken into account in the credit risk management and monitoring processes.

Sales / front office

As the direct point of contact for customers , the sales staff will be facing new challenges in the future but will also be afforded new opportunities. They must explain the necessary background to customers in an appropriate manner, collect the data and then feed it into the institution’s data infrastructure. The front office can then use this data in the lending process to draw conclusions about the sustainability risks of borrowers or investments.

The new ESG data requirements also open up additional opportunities for discussion topics and occasions and generate new sales impulses. For example, ESG-specific information can be used to make adjustments to the product portfolio and pricing, and ideally, to discuss with the customer the necessary adjustment and transformation paths. In principle, we can expect the transformation of the economy and society to generate enormous financing potential.

Sustainability changes banking for good

Customers, highly ready to change banks, are pushing the transformation: consumers are becoming more and more aware of sustainability, and this is increasingly influencing their consumption behavior.