|

Getting your Trinity Audio player ready...

|

A need for trade finance innovation

Although international trade recovered quickly after the post-Lehman Brothers crisis, the total volume of international trade flows has been fluctuating around pre-crisis levels over the last years. International trade prospects, however, are positive and a stable annual growth rate of around 2.4% is forecast for the medium term.[2]

Figure 1: International trade & traditional trade finance: historical volumes

Figure 1: International trade & traditional trade finance: historical volumesDespite the increase in international trade, banks are pessimistic about the overall traditional trade finance volumes and, as indicated in the ICC survey, do not expect any growth in the years ahead. As a result, the share of traditional trade finance in revenues is expected to fall to approx. 20% of the overall trade finance revenues by 2020.[3] Consequently, the role of traditional trade finance transactions, which currently account for around 50% of the banks’ revenues generated from trade finance, will be reduced in favor of open account trading.[4] Given that today traditional trade finance is the most profitable revenue source from international trade, banks will not be able to fully benefit from the growing volume of international trade.

There are several reasons why traditional trade finance has been losing importance, including improved legal security combined with easier communication between counterparties and access to information, all of which have reduced the need for trading risk mitigation instruments. Furthermore, traditional trade finance instruments were previously accessible to SMEs, which have begun to play a more important role in global value chains, than to large companies. This lack of access was mainly caused by high prices (resulting from processing costs), insufficient product knowledge and lack of necessary collateral.

In addition, increased regulatory burdens and compliance requirements have significantly raised the costs of traditional trade finance due to higher capital requirements and an expanded formal process, with the result that only parties conducting large transactions consider the use of traditional trade finance as a value-adding solution.

Finally, the main obstacle is the lack of end-to-end automation and digitalization. Processing traditional trade finance products, in particular letters of credit, still involves the exchange of paper documents and requires multiple manual activities and checks, which not only make it expensive for exporters and importers, but also error-prone. Customers also struggle with the lack of immediate and up-to-date insight into the transaction status and the ability to communicate directly with other parties involved in the process (freight forwarders, insurers, etc.).

So far, automation and digitalization initiatives have focused on reducing process costs and have concentrated on covering processes in core banking systems (i.e. mainly back-office processing), instead of actually digitalizing the entire trade finance transaction. Improvements that would eliminate the need for paper documents and introduce paperless trade finance processing (such as bank payment obligation, MT798 messaging, electronic bill of lading) are not widely accepted and their current use is limited.

The expected increase in global trade makes it attractive for trade financers to consider the application of new technologies that could provide a basis for innovative and cost-effective solutions. Among the emerging new technologies, distributed ledger technology (DLT) appears to be the most promising for redesigning the entire trade finance process, while other available solutions enable a significant operational improvement of existing processes.

Trade finance using DLT

DLT has several key features that make it potentially well-suited for building a trade finance platform. This technology offers peer-to-peer transactions, full transparency for all counterparties and instant access to information, thereby providing the ideal means for mitigating the current problems in trade finance.

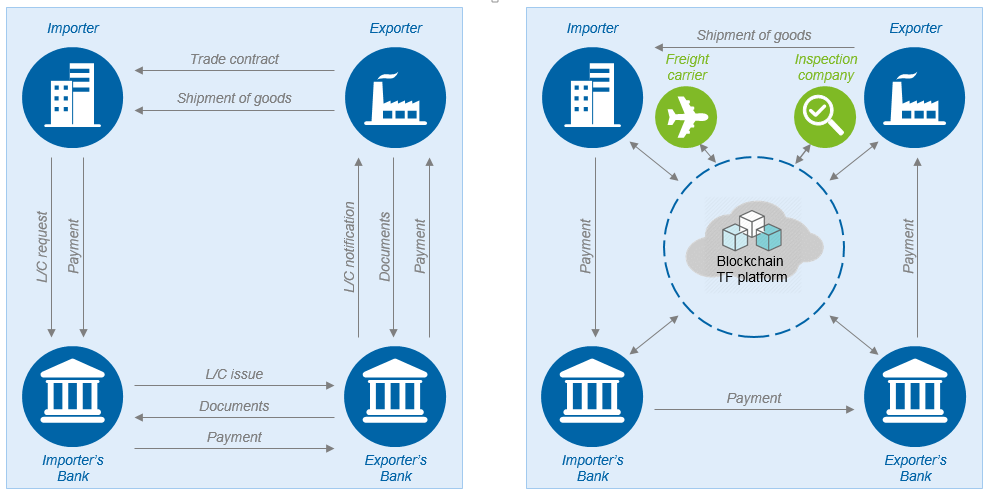

A trade finance solution built on DLT could support complete digitalization and end-to-end automation. Paperless processing is possible from the outset, i.e. both the definition and setup of contractual terms and conditions between exporter and importer as a smart contract on the DLT platform. A trade contract is subsequently shared with the importer bank and constitutes the basis for issuing a letter of credit (LoC), also in smart contract form on the platform. Approval of the LoC conditions, which is granted directly on the platform, triggers the shipping process. All parties involved (e.g. exporter, freight forwarders and freight insurers) add data and documents to the platform and confirm the execution or acceptance of each particular process step. After fulfilment of all LoC terms and conditions, payment is automatically triggered by a smart contract and initiated by the platform via API from the importer bank’s back office system.

The trade finance DLT solution offers various advantages for all parties involved. Banks, for example, benefit both from the elimination of manual tasks through process automation and self-fulfillment of deals, as well as from lower costs due to the redundancy of SWIFT messages, while simultaneously reducing operational risk associated with manual document checks. This solution also benefits both the exporter and the importer by enabling streamlined logistics processes, full transparency about the process status (e.g. current location and ownership of goods) as well as reducing risks and costs by minimizing errors. Since the need for paper document exchange and review is eliminated from the process, the time between shipment and payment is significantly reduced.

A number of advantages offered by a DLT-based trade finance platform inevitably make it a good candidate for future trade finance that could be widely adopted and used both by exporters and importers.

Figure 2: Current vs. future trade finance

Figure 2: Current vs. future trade financeThe development of trade finance platforms was carried out by several large banking consortia in collaboration with technology providers such as IBM Hyperledger or R3 Corda. Large institutions have opted for cooperation because these platforms can only be fully efficient and beneficial to customers if they reach a sufficient size and market coverage. The most advanced developments to date have been carried out by five consortia, namely we.Trade, Marco Polo, Voltron, Komgo and Hong Kong Trade Finance Platform. Although these initiatives seem promising, there are several factors which hamper the rapid expansion of these platforms: currently, only a few of them offer solutions designed for traditional trade finance (e.g. LoC), while others have decided to design solutions that only support open account trade transactions. Moreover, the process of integrating banks and other counterparties (i.e. inspection companies, freight forwarders, customs, etc.) from various countries into certain platforms requires time. It will take several years to reach a sufficient number of platform users. For this reason, DLT trade finance appears to be a rather distant solution with the potential to revolutionize trade finance, but only in the medium term.

Banks should nevertheless carry out a detailed assessment of existing platforms and, if attractive from a business perspective, join existing consortia and start developing these solutions further. It is, however, recommended that banks currently focus more on other technologies that are already available and which, by streamlining trade finance processes, can provide significant added value to banks and customers in the short term. Among these, the most well-known are optical character recognition, robotics process automation and workflows using machine learning algorithms.

Optical character recognition

OCR technology using artificial intelligence solutions could be a meaningful innovation in trade finance. Its key feature is to enable the conversion of paper documents or documents containing unstructured data into a selected electronic format and subsequently deriving transaction-relevant data in structured form. It is based on AI, which improves the scanning efficiency and can process a larger number of documents. Document processing with the OCR solution offers the user full recognition of characters or entire texts and then the selection of data contained in the document, based on key words. Some advanced OCR solutions may also offer compliance checks of data correctness against transaction conditions.

From a trade finance perspective, the most beneficial effect of OCR implementation is a significant reduction of working time (25–50% of processing time, depending on the process[5]) associated with paper-based document processing. The following example shows how OCR is applied in LoC processing, enables a direct comparison of extracted data with the LoC conditions and a quick identification of any discrepancies and reduction of time required to perform this process.

Figure 3: OCR in LoC processing

Figure 3: OCR in LoC processingRobotics process automation

Robotics process automation (RPA) is another technology that could significantly improve trade finance processes. It enables full process automation based on the implementation of software imitating the activities performed by the employee and eliminates manual operations such as data entry or saving and uploading documents. In addition, there is no need to integrate systems and rebuild IT architecture; the robot accesses the system and processes the data in the same way as an employee. RPA can be used for specific process steps and enables increased efficiency, a better data quality and a reduced risk of potential errors. As a consequence, RPA application is simple, relatively cheap and quick to fully implement.

It is important to keep in mind that not all processes qualify as RPA candidates. Only structured, repetitive and rule-based processes are eligible, such as monitoring newly received documents, converting scanned documents, classifying documents, extracting data and performing compliance checks.

Figure 4: Robotics process automation (RPA)

Figure 4: Robotics process automation (RPA)Workflow

Last but not least, workflow is another solution capable of supporting trade finance automation, especially in the processing of trade finance product applications. Key benefits of the workflow solution lie in the automated and direct distribution of tasks to persons responsible for the individual process steps, the efficient flow of information and documents between process participants and systems, as well as in real-time process monitoring and control.

Moreover, workflow combined with solutions using machine learning could help to address complex topics, such as scoring models for SME customers applying for trade finance products. Not only would this streamline the processing of trade finance product applications, but it would also allow the extension of trade finance offerings to SME customers who, under current methodologies, would not be considered creditworthy.

Figure 5: Workflow solution

Figure 5: Workflow solutionConclusions

Traditional trade finance has reached a turning point. Despite the growing volume of international trade, the total volume of traditional trade finance remains stagnant without signs of further growth. In order to reverse this trend and to capitalize on growing international trade, banks should consider innovations in trade finance by implementing new automation and digitalization solutions. While DLT appears to be a game changer in the longer term, for the time being banks should focus on the solutions currently available and take a 4-step approach:

- Analyze their status quo and identify major pain points in trade finance from a service, product and operational perspective

- Define their future trade finance positioning, including target customer segments and service offerings along with a clear set of KPIs that improve the definition of objectives

- Identify and evaluate available technological solutions that could enable a quick trade finance transformation towards the target image and ambition level

- Select the most suitable solutions and promote their implementation

One response to “Innovations in trade finance”

dhriti

well informed.