|

Getting your Trinity Audio player ready...

|

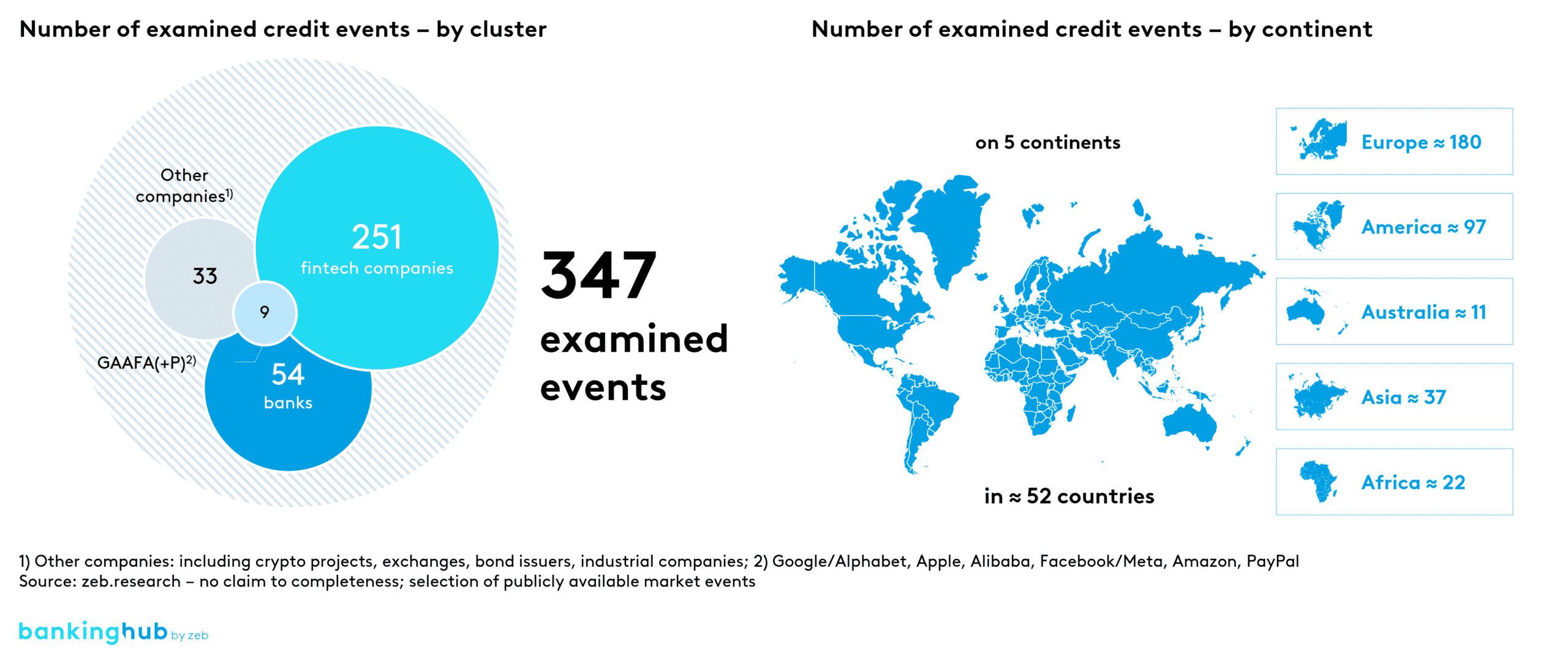

Credit events: a global perspective

In our review of the 2022 lending business, we examined credit events and trends around the world on the basis of prestigious German and international newsletters (Finanz-Szene, Finextra, Der Treasurer and many more), as well as news and corporate websites. This allowed us to identify 347 events in 52 countries on 5 continents for the year 2022.

Data-driven lending (DDL)[1]

In the past few years, there have already been quite a few events related to data-driven lending, and there will likely be more in the years to come. In 2022, artificial intelligence and machine learning (ML) were increasingly used in the lending business to issue individualized loan offers as well as to rate creditworthiness or perform debt servicing capability checks based on alternative data (mobile phone data, social media, etc.).

AI has various applications along the lending process, some of which are already in use (see “Document verification: detecting fraud using AI”, German version only, English version coming soon)

Lending platforms and ecosystems

Lending platforms and ecosystems remain prevalent topics. With the various platforms around (comparison platforms, sales platforms and credit marketplaces), financial institutions are challenged to develop their own solutions or to cooperate with platform providers, for example via embedded finance.

Buy Now, Pay Later (BNPL)[2]

In 2022, there were many events in the BNPL business. A significant proportion of these events is accounted for by the funding rounds of fintech companies willing to enter the BNPL business, or of established players that have not been actively promoting BNPL before (e.g. Apple). There were also some acquisitions and consolidations. In the context of current developments, the future prospects of the BNPL market are very exciting.

Decentralized finance lending[3]

Decentralized finance, in particular decentralized lending, was strongly affected by the 2022 crypto market downturn. Accordingly, there was only a small number of credit events to be identified in that area.

Due to various fraud scandals and cyber attacks, the overall trust in cryptocurrencies has been shaken. Nevertheless, we see great potential in blockchain technology and smart contracts, especially in terms of decentralized lending.